You can replace this text by going to "Layout" and then "Page Elements" section. Edit " About "

Pague com LPs do Mister Colibri

Quer comprar celular,Tablet,pen drive, GPS e muito outros produtos e ainda podendo pagar tudo em LPs ?Pois saiba que isso é possível,basta você visitar o site downloadstotal.com e realizar a sua compra com toda tranquilidade e segurança!!!

Ali Ghodsi is taking aim at giants. The Databricks CEO is no longer just sniping at $60 billion competitor Snowflake, but has ambitions for his company to be as big as $300 billion Salesforce, according to Jon Victor's profile on the everywhere-at-once computer science professor. Reading the piece, I couldn't help but think about the potential battles to come between the blunt Ghodsi ("I've heard the whole range of opinions on my opinions," he quipped) and Salesforce's gregarious leader, Marc Benioff. The two companies are just starting to go head to head over a differing vision of how companies should access, label and make sense of their data—Databricks versus Salesforce's Data Cloud. How that battle plays out has lucrative implications. Even setting up the rivalry this way is flattering to Databricks—an acknowledgment that it is among the big boys of software, just a couple years after surpassing $1 billion in annual sales. More investors are starting to believe in Databricks' future as it updates its financial performance while fundraising for the largest private financing round in history, at a $60 billion–plus valuation.

Dec 3, 2024

Dealmaker

By Cory Weinberg

You're receiving Dealmaker for free. Upgrade to a paid subscription to access all of our award-winning tech and business journalism. Subscribe to The Information here for 25% off your first year (normally $399).

Welcome back!

Ali Ghodsi is taking aim at giants. The Databricks CEO is no longer just sniping at $60 billion competitor Snowflake, but has ambitions for his company to be as big as $300 billion Salesforce, according to Jon Victor's profile on the everywhere-at-once computer science professor.

Reading the piece, I couldn't help but think about the potential battles to come between the blunt Ghodsi ("I've heard the whole range of opinions on my opinions," he quipped) and Salesforce's gregarious leader, Marc Benioff. The two companies are just starting to go head to head over a differing vision of how companies should access, label and make sense of their data—Databricks versus Salesforce's Data Cloud. How that battle plays out has lucrative implications.

Even setting up the rivalry this way is flattering to Databricks—an acknowledgment that it is among the big boys of software, just a couple years after surpassing $1 billion in annual sales. More investors are starting to believe in Databricks' future as it updates its financial performance while fundraising for the largest private financing round in history, at a $60 billion–plus valuation.

'Rule of 52'

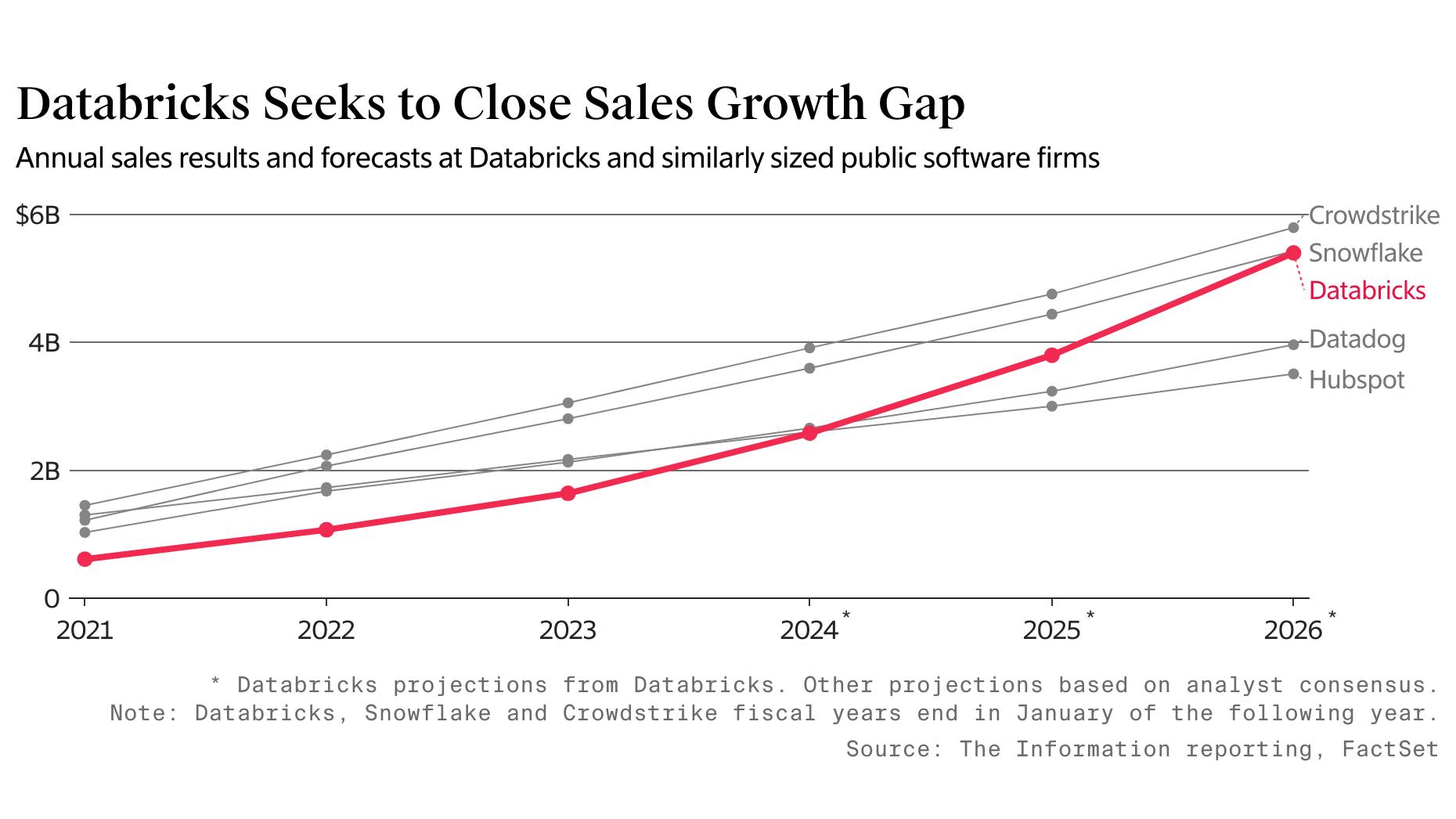

Those updates reveal that Databricks is beating its own forecasts from last year, which I wrote about then. It is now forecasting nearly $2.6 billion in revenue this fiscal year, which ends in January 2025, a 57% annual growth rate on the year to last January. That total is about 3% higher than what it had originally forecast. Doing slightly better than what you said you're going to do always makes investors happy.

Moreover, Databricks recently told investors it expects its sales to grow more than 40% each of the next two years as well, putting it at about $5.4 billion in sales by the year that ends in January 2027. That would make it as big as Snowflake that year, according to FactSet estimates. If Databricks hits that number, investors would be valuing the company this fundraising round at about 11.5 times that year's sales, about a point higher than where Snowflake currently trades.

Databricks is an outlier in an important way among software giants, however: It isn't profitable. Of the dozen or so publicly traded software firms valued over $50 billion, each has a double-digit free cash flow margin. Databricks, on the other hand, expects to burn about $140 million this year, for a negative 5% free cash flow margin. I should note, however, that this cash burn is significantly lower than what it had expected last year. (A Databricks spokesperson declined to comment.)

That cash burn is the result of the company going into investment mode over the last few years—competing with big tech firms over top engineers and building up its sales ranks—as many software firms pulled back. Its fast pace of growth seems to justify the investment, if you use the same "Rule of 40" framework—free cash flow margin plus revenue growth—that many software investors rely on. Databricks' growth rate of 57%, minus its negative free cash flow margin, amounts to about 52%, only slightly lower than what Datadog, CrowdStrike and Snowflake expect, according to FactSet estimates.

Who does Databricks significantly surpass with that figure? Salesforce, which is at about 40%.

Wealthfront's Future

It always struck me as a cruel contrast that a company like Robinhood grew to become a $30 billion–plus phenomenon on the back of cheap options trading that makes stock picking feel like a videogame for millennials.

Meanwhile, the likes of Betterment and Wealthfront—more risk-averse robo advisers that tout financial goal setting, diversification and high-yield savings accounts—have plodded along and struggled to break through. Quietly, however, 16-year-old Wealthfront may be a sleeper candidate for an interesting consumer fintech initial public offering next year, particularly if bigger IPO candidates like Chime and Klarna do well.

Wealthfront's fortunes appear to be rising: The firm recently bought back some stock from employees at a price that implies a $2 billion valuation for the company. That's up from the $1.4 billion UBS agreed to pay for the startup in January 2022, before scrapping the deal a few months later.

David Fortunato, Wealthfront's CEO, told me recently that the company will generate about $290 million in revenue this year, with more than $100 million in free cash flow. It's taken advantage of a couple years of high interest rates to attract new customers looking for some extra yield on their cash, getting them to switch from Chase or Wells Fargo. The startup's marketing budget and hiring pace are up this year, as is revenue growth.

Fortunato didn't comment directly on an IPO, but he pushed back when I raised the issue that the firm's revenue seemed too small for going public, based on some tech investors' conventional wisdom. "There's a lot of book talking that occurs. A lot of the people that are promoting that companies need to be larger are investors in late-stage rounds that need to invest in late-stage companies that are private," he said. "It's in their financial interest for that to be the case."

What's in Fortunato's financial interest is the message that Wealthfront's best days are in front of it. He said the company likes to talk about how investing behemoth Charles Schwab took decades to build, too. "It takes some time to build businesses that have a great deal of client trust and manage a large percentage of people's assets for them," he said.

Tech IPO Watch

ServiceTitan's IPO road-show video is out today, and the company is likely (if all goes smoothly) to ring the bell at Nasdaq next week.

The video, as always, is a pricey piece of high-stakes marketing. But it reminded me why IPOs are fun: Companies get to tell a story, not just with GAAP numbers but with words and images. ServiceTitan's story is compelling as vertical software companies focused on electricians and landscapers go. "Tradespeople are caretakers," the video starts. "They give you heat, they cool you down, they keep the lights on."

How well the story holds up is what investors (and journalists) need to probe. The company said in its IPO prospectus it is hoping to sell as much as 8.8 million shares at as much as $57 a share, valuing the company as high as $5.2 billion.

Founders Fund Move

Founders Fund, one of Silicon Valley's premier venture firms, started the year with five general partners. It's down to three.

Brian Singerman, a long-tenured Founders Fund leader, said today he is stepping back—nearly one year after general partner Keith Rabois decamped for his prior employer, Khosla Ventures. The new emeritus role means Singerman won't vote on other partners' deals, but he can bring deals to the partnership and lead those rounds, according to a spokesperson

The latest departure is sure to fire up more palace intrigue. Trae Stephens, a general partner that Natasha profiled earlier this year, represents the new generation of Founders Fund. But, at the end of the day, this is Peter Thiel's firm. Everyone else is a supporting character.—Natasha Mascarenhas

More than 100,000 subscribers rely on The Information's Creator Economy newsletter for insightful coverage on creator startups making waves, big tech companies' social media playbooks, and scoops on the biggest hires across the sector. Start receiving the weekly newsletterhere.

Join us for a discussion on the evolving role of AI in driving ROI across industries. Hear from top AI experts and business leaders about how companies are applying this technology and gain insights into what's working today and what's next for 2025.

Venture capital is at a crossroads. Reporters Cory Weinberg and Natasha Mascarenhas tell you what's coming next, who's winning—and who's losing—in the high-stakes world of startup investing.

0 comentários:

Postar um comentário