A Reuters Open Interest newsletter |

|

|

What matters in U.S. and global markets today |

By Marc Jones, Senior Global Markets Correspondent |

|

|

The slump in gold, silver and other precious metals is continuing to rattle global markets and making for a nervous start to the month. After Kevin Warsh's on Friday, a potent mix of margin calls, momentum selling and - at least for now - a dialing down of U.S.-Iran sabre-rattling appears to be fueling ongoing volatility in the one part of the market most prized for its safety. There is a lot of red on the screens out there again and that is ahead of a week packed with corporate earnings, central bank meetings and major economic data, starting with ISM numbers out later. I'll get into all the market news below. But first, check out Mike Dolan's latest column below on why the Warsh-Trump pairing may not be a match made in heaven. And listen to the latest episode of the Morning Bid daily podcast. Subscribe to hear Reuters journalists discuss the biggest news in markets and finance seven days a week. |

|

|

- Commodities markets slumped on Monday, led by deep losses in gold, silver, oil and industrial metals, as the choice of Kevin Warsh as the next Fed chair .

- Oil prices fell nearly 5% on Monday after U.S. President Donald Trump said Iran was "seriously talking" with Washington, signalling .

- Japanese Prime Minister Sanae Takaichi's party is likely to score a landslide victory in next week's lower house election, .

- OPEC+ will struggle to control the two likely determinants of crude prices in the near term. Find out what they are in the latest piece from .

- Chinese exports of copper, zinc, and nickel soared in 2025 amid tariff-driven arbitrage and China's growing processing capacity. This could be a signal of more turmoil ahead for base metals, .

| |

|

Having zoomed up on the escalator, the worry is now that gold and silver markets are hurtling down in the lift as investors unwind their trades. Silver is currently down another 5.5% and after Friday's 30% plunge is headed for its biggest two-day loss since at least the 1980s. Gold has dropped another 3.4% too after its 9% Friday meltdown marked its biggest single-day decline since 2013. Dealers say pressure on a number of silver futures funds in China added to the rout late last week and the mood hasn't been helped today by news that CME had raised margin calls on some of its key gold and silver futures contracts. Adding to the commodity crunch, oil prices are also down nearly 5% after Trump said over the weekend that Iran was "seriously talking" with Washington, perhaps lessening the risk of a U.S. military strike on the country, at least in the coming days. It has all started to knock the equity markets. Wall Street's Nasdaq futures are off nearly 1% while the so-called VIX "fear gauge" is rising toward the 20 level again. About one quarter of the S&P 500 is set to report this week, and growth in earnings per share was running at 11% on the previous year, when consensus had been for 7%. Scrutiny will be razor sharp on tech majors Alphabet, Amazon and AMD, particularly on their costs and how they see the benefits of AI in the wake of Microsoft's poorly received results last week. European stocks are showing some signs of stabilisation - around 30% of the STOXX 600's constituents report earnings this week. But Asia saw the "bubbly" South Korean stock market tumble 5.5% as its big name chipmakers got whacked by the persistent AI jitters and Hong Kong's Hang Seng also fell over 2% after data over the weekend revealed China's official PMI fell back below 50 again. Japan's Nikkei also dropped more than 1% despite a brief push into the green on an opinion poll suggesting Prime Minister Sanae Takaichi's Liberal Democratic Party was likely to score a landslide victory in next week's lower house election. The coming week also has a deluge of U.S. macro data. Monday kicks things off with the January ISM manufacturing index although the main event will be Friday's non-farm payrolls report, with consumer sentiment figures and the latest Treasury's quarterly refunding details keeping the interest up in between. Also on the menu are policy meetings by the Reserve Bank of Australia, European Central Bank and Bank of England. The RBA is an outlier in that markets imply around a 75% chance it will raise interest rates by a quarter point to 3.85%, so reversing one of three cuts delivered last year, in an attempt to quell resurgent inflation. |

How soon before Trump dubs Kevin Warsh 'clueless'?: Mike Dolan |

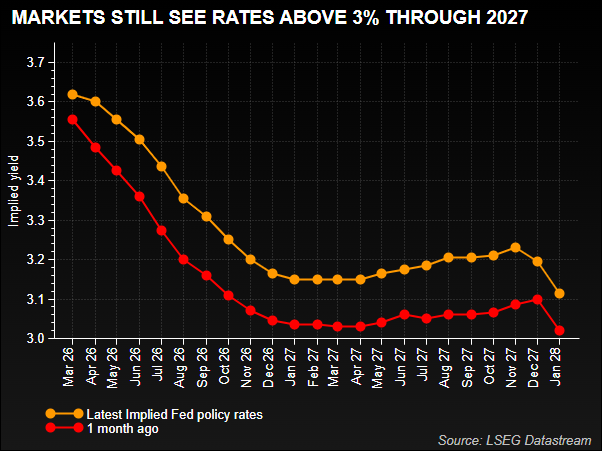

In many ways President Donald Trump's decision to pick former Federal Reserve governor Kevin Warsh to head the central bank is a relatively orthodox choice. To many, he is not the ardent interest rate slasher the U.S. president seemed to want. But maybe Trump is just happy having a scapegoat at the Fed. It took less than six months between Trump appointing current Fed Chair Jerome Powell in late 2017 - after endorsing him as someone with "considerable talent and experience" - and then publicly regretting the choice as interest rates climbed. A year later he was calling Powell "clueless." Since Trump's return to the White House last year, the insults have worsened, with threats to fire him and even talk of a potential criminal indictment — all coming even as rates fell, in the president's view, "too late." Will it be different this time? Trump announced on Friday that Warsh was his candidate to lead the Fed, ending months of interviews and teasing amid widespread political and investor hand-wringing over whether the once fiercely independent central bank is being politically captured. But the initial market reaction to the decision, which still needs congressional confirmation, was modest. With a blizzard of other domestic and global influences swirling, it was hard to detect any sudden or pointed shift in the dollar, Treasury bonds or stocks that indicated fresh anxiety. A basic test of that was that futures still pointed to roughly two Fed rate cuts in 2026 — about where they've been since last year. The shaky dollar firmed a bit on the news, and the Treasury yield curve steepened slightly. |

Graphics are produced by Reuters. |

|

|

Graphics are produced by Reuters. |

It's worth acknowledging that despite the severity of the gold and silver routs, they remain comfortably higher than the already lofty positions at which they started the year. They raced higher when Washington captured Venezuelan President Nicolas Maduro and then a major row blew up with Europe about Trump's proposed grab for Greenland. While that rally has hit the buffers for now, it could just be a timely correction. Deutsche Bank on Monday said it still saw the case for a gold price of $6,000 an ounce given the uncertain global outlook and European defence stocks are also still firmly in vogue. On the flip side, the dollar has risen for the last couple of days as Warsh's nomination for the Fed job has eased some of the more extreme worries about the U.S. central bank's cherished independence. And its strength - or lack of it - remains crucial for all kinds of markets. |

- U.S. January ISM index (10:00 AM EST)

- Canada January manufacturing PMI (9:30 AM EST)

- Fed's Bostic speaks, BoE's Breeden speaks

- U.S. corporate earnings: Palantir, Walt Disney

|

|

|

Want more smart, engaging financial analysis in your inbox? Subscribe to Trading Day by Jamie McGeever, a daily newsletter delivered just after the market close. And check out Reuters Open Interest (ROI), an essential new source for data-driven, expert commentary on market and economic trends. You can find ROI on the Reuters website, and you can follow us on LinkedIn and X. |

Opinions expressed are those of the author. They do not reflect the views of Reuters News, which, under the Trust Principles, is committed to integrity, independence, and freedom from bias. |

Morning Bid is sent every weekday morning. Think your friend or colleague should know about us? Forward this newsletter to them. They can also sign up here. Want to stop receiving this email? Unsubscribe here. To manage which newsletters you're signed up for, click here. This email includes limited tracking for Reuters to understand whether you've engaged with its contents. For more information on how we process your personal information and your rights, please see our Privacy Statement. Terms & Conditions |

|

|

|

|

0 comentários:

Postar um comentário