You can replace this text by going to "Layout" and then "Page Elements" section. Edit " About "

Pague com LPs do Mister Colibri

Quer comprar celular,Tablet,pen drive, GPS e muito outros produtos e ainda podendo pagar tudo em LPs ?Pois saiba que isso é possível,basta você visitar o site downloadstotal.com e realizar a sua compra com toda tranquilidade e segurança!!!

Startup investors have been scurrying lately to come up with new ways to turn their investments into cash, given that the conventional paths to cashing out—the startup goes public or gets acquired by a bigger tech firm—are much harder to pull off nowadays. Some investors are hoping private equity firms snap up their companies. Others are trying to find willing buyers for their stakes in the secondary markets. ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏ ͏

Sep 23, 2024

Special Report

By Cory Weinberg

Supported by

Welcome to the third edition of our M&A newsletter, part of The Information's expanded finance coverage. We publish this newsletter throughout the year, with the aim of keeping you up to date with the biggest trends in mergers and acquisitions.

Startup investors have been scurrying lately to come up with new ways to turn their investments into cash, given that the conventional paths to cashing out—the startup goes public or gets acquired by a bigger tech firm—are much harder to pull off nowadays. Some investors are hoping private equity firms snap up their companies. Others are trying to find willing buyers for their stakes in the secondary markets.

Then there's this more controversial idea: tech investment bankers at some smaller banks, deep into their third straight year of deadened IPO activity, are trying to gin up enthusiasm for taking even a relatively small firm public.

The advice cuts against a longstanding belief that companies that are too small—say, under a billion-dollar market cap—struggle on the public markets. They're too small for the mutual funds that dominate investments, and they don't get the attention of Wall Street research analysts, which is seen as necessary to put companies on investors' radar. As Coatue Management's Phillippe Laffont said at our Private Capital Conference in April, companies need at least $1 billion in sales to go public.

But the idea that small companies could try the public markets may have new life after the Federal Reserve's interest rate cut last week, which should help drive higher valuations for fast-growing tech firms, even small ones.

Carl Chiou, head of West Coast equity capital markets at William Blair, wrote some tactical advice to clients this summer. He suggested that smaller companies have a couple of options to help them go public, beyond figuring out how to hasten their growth rates or buying other companies to get bigger.

One option is to sell more shares in the IPO than the usual 10% to 15% of the company's outstanding shares. Doing so would dilute the stakes of existing shareholders more, but at least it would get the company public and make their stakes more liquid, he argued. One company that used this strategy was Silvaco, a 40-year-old semiconductor software company with only about $54 million in revenue last year, which sold nearly a quarter of the company in the IPO. (Its stock is down about 20% from its May IPO, however.)

Another option, he wrote, is to identify investors who run smaller funds as well as individual investors. "These two groups can speak for significant percentages of smaller-cap IPO allocations," he wrote.

Tech bankers at RBC Capital Markets wrote to clients this month that investors care more about a company's ability to hit the numbers it says it will reach once it goes public, than how big it is. A company's long-term growth potential also matters more than size, as long as the company goes public selling at least $100 million of float and at least a $1 billion market cap, they argue.

Among U.S. tech firms that have gone public since 2020, RBC found no correlation between revenue scale and how companies' stock performs. In that list, strong performers with less than $500 million in revenue the year following their IPOs include Monday.com, Datadog, CrowdStrike and Zscaler.

That list, however, didn't include companies that went public via special purpose acquisition companies. That's the regretful route many small, struggling venture capital–backed companies such as BuzzFeed, Sonder and Nextdoor took.

Whether the small-cap IPO idea actually has legs is more of a narrative to watch for next year. Tech IPO activity is likely to be fairly quiet the rest of the year, with some possible exceptions such as Nvidia challenger Cerebras and Sequoia Capital–backed ServiceTitan, which sells software for landscapers and plumbers. That defies banker predictions that the second half of this year would be busier with listings.

What will really spark an IPO revival? Businesses big or small that actually perform really well, said Becky Steinthal, Jefferies' head of tech, media and telecom equity capital markets. "I don't have investors telling me anymore they're closed for business. They just are not interested in businesses facing existential crises," she said.

"Yes, it's hard to get a smaller-cap IPO done. The bar is higher for investors to spend time on it," she added. "But a good business will do very well, and you'll be able to get a story in front of the right investors on a company of any size."

The Great DTC Unwinding

Consumer product giants that expanded through frequent acquisitions in recent years are now reversing course, ditching online brands and other once-trendy bets to focus on boosting margins in their core businesses.

This month, General Mills announced it would sell its North American yogurt businesses for $2.1 billion to two privately held dairy firms. In June, pharmaceutical giant Bayer said it would stop investing in its majority-owned subsidiary online supplement brand Care/of, prompting the brand to wind down. And last November, Unilever sold Dollar Shave Club, a direct-to-consumer razor company it originally bought for $1 billion in 2016, to private equity firm Nexus Capital Management.

"There's a very big push on corporates to be focused in their approach right now," said Brandon Yoshimura, a director at Solomon Partners who has advised on divestitures involving direct-to-consumer brands.

That unwinding is likely to continue in the coming months. Buyers could include firms that specialize in brand licensing and distressed retailers.

Those firms have been active lately. Consortium Brand Partners acquired athleisure startup Outdoor Voices earlier this year, and CSC Generation Enterprise, which owns Sur La Table and One Kings Lane, bought online outdoor retailer Backcountry this month from private equity firm TSG Consumer Partners.

Such firms, which tend to be backed by private equity or venture firms, typically snap up brands bigger companies are discarding at a discount. For example, Walmart sold Bonobos' intellectual property for $50 million to WHP Global in 2023, six years after paying $310 million for the menswear maker. (Retailer Express paid Walmart another $25 million for Bonobos' operating assets.)

It's also possible a startup founder will buy back their firm from the company they sold it to. That's already started to happen: Earlier this month, Cassandra Grey, founder of Violet Grey, bought the direct-to-consumer beauty company back from Farfetch, the luxury goods site. Farfetch bought Violet Grey in early 2022 for more than $50 million to expand into beauty. Since then, however, Coupang acquired Farfetch itself in late 2023.

With most big consumer companies looking to slim down rather than pursue more acquisitions, private consumer companies looking to either sell or go public are in a holding pattern given the still-icy IPO market. But if high-profile IPO hopefuls like Skims or Vuori do make it to public markets next year, that should serve as a reset that could make acquirers more confident they're paying a reasonable price.

"That'll be really helpful to price things in the private market from an M&A perspective," Yoshimura said of a consumer IPO market comeback.—Ann Gehan

Quiet on the Deal Front

Chart by Shane Burke

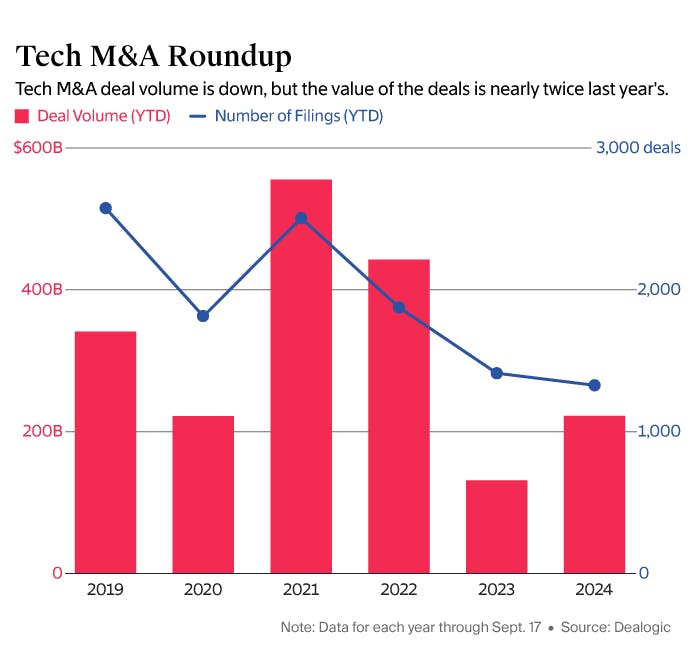

It's not your imagination. Deal activity in the tech sector remains muted, according to data from Dealogic, although the dollar value of deals getting done is up compared with the same time last year.

So far this year, the number of deals announced year to date was 1,325, the lowest number since at least 2019 and down nearly half from 2021. But the dollar value of these deals was $222 billion, which is up 69% from last year. (See chart above).

Dealogic's data cover deals that have been announced during the period, even if they haven't closed, and only include deals where a tech company is the target. That means we're not including deals such as Verizon's recently announced purchase of telecom firm Frontier, or Silver Lake's buyout of entertainment conglomerate Endeavor.

Private equity firms did the vast majority of the tech deals, such as Permira's $7.2 billion acquisition of Squarespace, which sells online marketing tools to businesses. The firms were on both sides of some transactions—Bain Capital is acquiring PowerSchool, which is partly owned by Vista Equity Partners, while KKR and Dragoneer Investment Group are buying Instructure Holdings, which is majority owned by Thoma Bravo.

The tougher antitrust regime in both the U.S. and Europe continues to limit the number of acquisitions tech companies are doing, although some are getting through. Hewlett Packard Enterprise, for instance, has received European regulatory approval for its $14 billion purchase of Juniper Networks and expects to close the purchase by the end of this year or early in 2025.

Another factor, of course, is high interest rates. And while the Federal Reserve's cut last week signals that rates are starting to come down, there's little hope that things will improve anytime soon.

"I think it's going to be a tough market for another five or six months at least," said Annie Nazarian Davydov, a partner in Lowenstein Sandler's transactions and advisory group. "I'd be surprised if we even saw in the first quarter of 2025 some pick up, but I don't expect it to be like 2020 for another several years."

Davydov noted that "everyone was expecting" the Fed's rate cut, "so it's kind of been priced in for the last few months anyways."

Moreover, she noted that plenty of companies—at least in the private equity sphere—have the money to do deals. "It's just a matter of what are the valuations on the assets and how much is the interest on the debt, and I think both are still too high.…One of those has to go down a little bit more before we see more action."—Martin Peers and Ann Gehan

0 comentários:

Postar um comentário