Hi there,

Happy July 4 weekend to all those who will soon be celebrating – and greetings to Reuters Tariff Watch subscribers who have switched over to Econ World. Welcome!

We kick off in Ukraine, where Russia grabbed the headlines with its most intense attack on Kyiv so far this year. The deadly show of force killed at least 18 people in Ukraine’s capital and forced thousands to flee. Moscow said the barrage was in retaliation for Ukrainian drone strikes.

Those attacks on fuel facilities deep inside Russia have brought the war to President Vladimir Putin’s doorstep. Widespread fuel shortages are disrupting daily life in one of the world’s biggest petrostates. In some regions, retail gasoline prices have risen to some of the highest levels in Europe, bus routes have been cancelled and frustration over long lines at gas stations has led to fist fights.

Even before the shortages escalated last month, Russians were feeling more pessimistic about economic conditions than at any time in the past 20 years. Higher energy prices will add to the gloominess, further fuelling inflation and putting consumers and businesses under even more pressure in a spluttering economy.

A report from the Kiel Institute for the World Economy says that Russia is showing signs of “structural exhaustion”. Russia’s fiscal position has been deteriorating but the problems are not yet acute. In the first five months of the year, Russia ran a budget deficit of 2.6% of gross domestic product, above an annual target of 1.6% of GDP due to increased military spending. But the increase in borrowing this year is not as big as last year and Moscow still has ample rainy day funds to dip into. Inflation, while still over 5%, is half its recent peak.

Over in the Gulf, oil and gas producers are boosting shipments following an interim peace deal between Washington and Tehran. But are they getting out while the going is good? Iran is determined to keep controlover the Strait of Hormuz. Under the terms of the interim deal, Iran agreed to let ships pass through it for 60 days without charge and it wants formal acceptance of its control of the Strait recognised. If the interim deal ends without being extended, Iran would start charging ships for passage in mid-August.

It’s no wonder then that Gulf states are scrambling to find ways to circumvent the strait to get their energy exports out. Pipeline mania is all the rage in the region, according to Timour Azhari, Reuters chief correspondent in Saudi Arabia. I talk to him on this week’s Reuters Econ World podcast about the geopolitics at play in this diversification drive. Watch it here.

U.S. job growth slowed more than expected in June and data for the prior month was revised lower, but the unemployment rate fell to 4.2%, pointing to continued labor market stability.

Investors’ initial assumption that new Fed Chair Kevin Warsh will quickly cut rates has evaporated. Warsh said this week that he will stick firmly to the U.S. central bank's 2% inflation target and "disappoint" anyone who expects loose monetary policy.

Over three days at the European Central Bank's annual gathering in Sintra, Portugal, the new Fed chair held a series of private meetings with counterparts from Europe and beyond, reassuring them about future relations. He also found allies in his preference for simpler messaging and scepticism towards forward guidance.

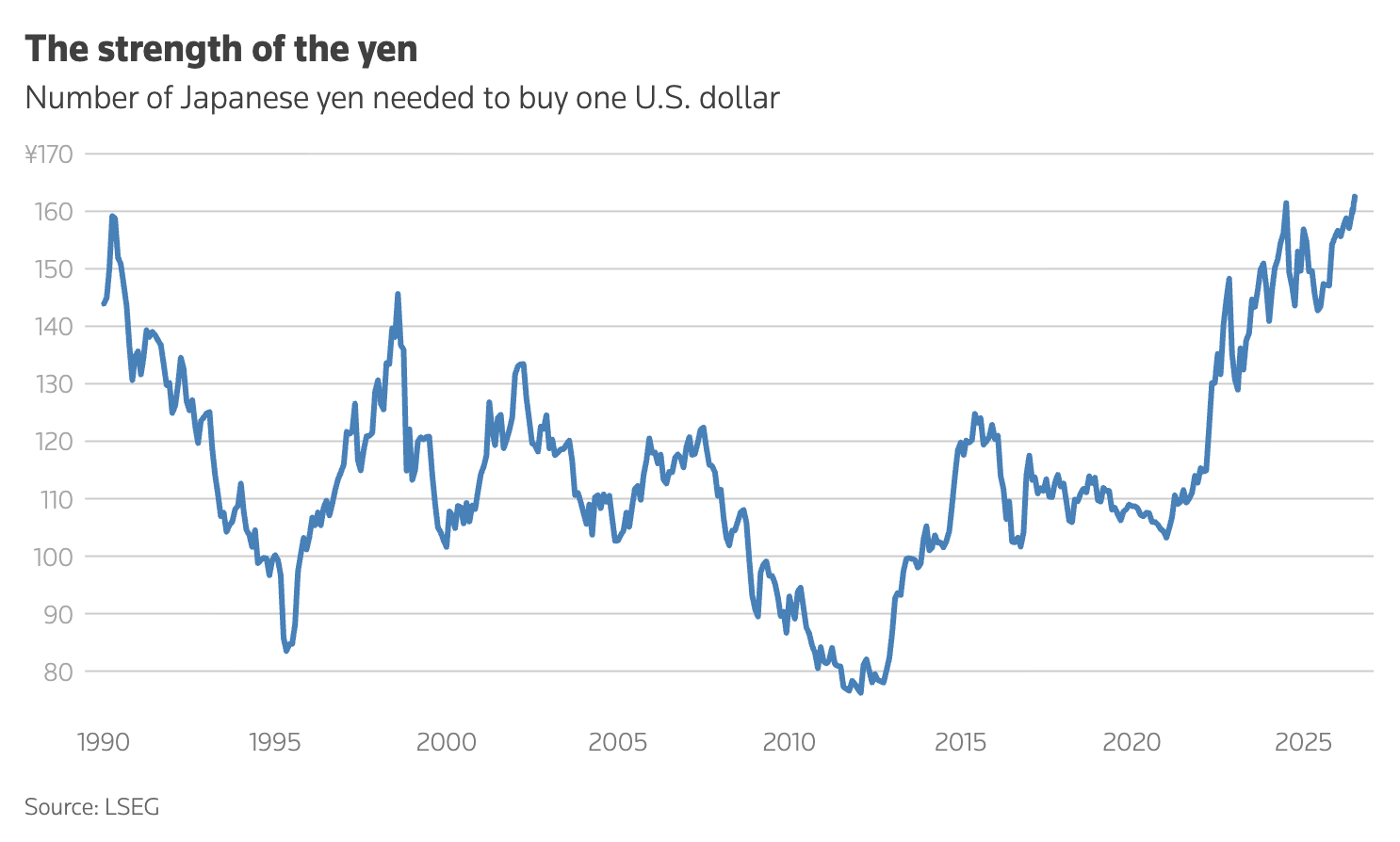

Japan’s Ministry of Finance (MOF) is echoing Warsh’s preference for silence. With the yen at 40-year lows, MOF officials are abandoning their habit of telegraphing intervention risks, instead signalling a more targeted campaign to squeeze speculators and raise the cost of betting against the battered yen. The shift reflects a more aggressive approach by the MOF and raises the risk of a surprise intervention. Keep your eyes peeled for any sharp yen moves over this U.S. holiday weekend.

And a service announcement that next week’s newsletter will land on Wednesday instead of Thursday.

If you have any feedback for me drop me a link on LinkedIn.

0 comentários:

Postar um comentário